On-Behalf Payments¶

About this guide

Installation requirements

In freight forwarding, it is common for the forwarder to advance payment or collect on behalf of the customer for charges that are ultimately the customer's obligation: port handling fees, container detention, customs duties, quarantine, fumigation, or amounts billed directly by the carrier or port authority per the original document. These amounts are not the forwarder's service revenue — they are pass-through funds that the customer must reimburse, dollar for dollar.

Treating pass-through charges as service revenue inflates gross profit and creates a false picture of the shipment's performance. Treating them as service cost deflates it just as badly. The On-Behalf Payment feature creates a third category that keeps pass-through money separate from both.

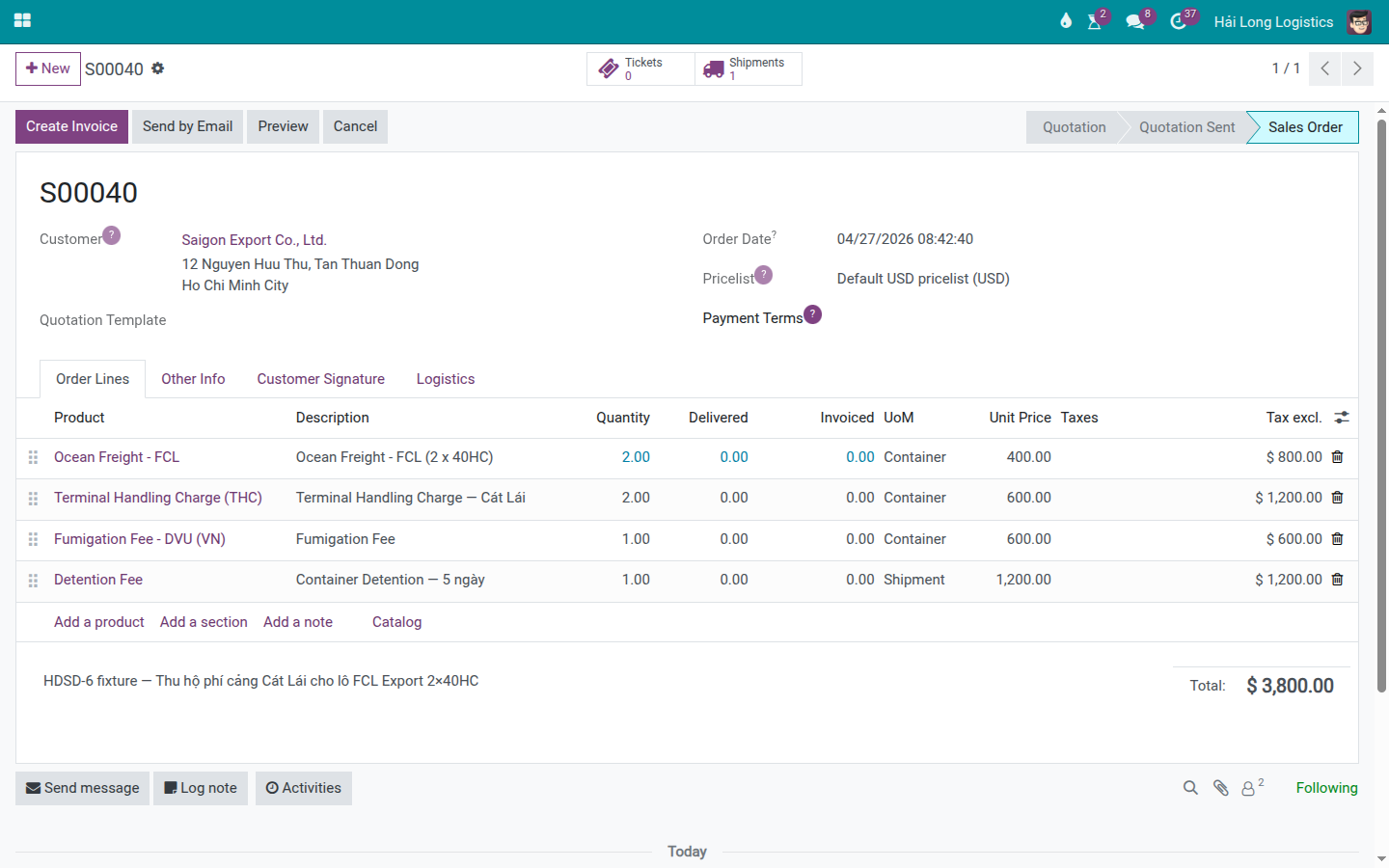

Scenario thread: Hai Long Logistics is processing a sea FCL export for Saigon Export Co., Ltd. at Cat Lai port. In addition to Ocean Freight (which has a markup and is Hai Long's service revenue), the customer has asked Hai Long to advance three port-side charges: THC USD 1,200, Fumigation USD 600, Container Detention USD 1,200. Total advance: USD 3,000. Hai Long needs to recover exactly USD 3,000 from the customer — and this recovery must not appear as service margin in the shipment's gross profit.

Xem thêm

Freight terminology (THC, DEM (Demurrage), DET (Detention), Incoterms, Gross Profit): Industry Glossary.

When to use this guide¶

Use this guide whenever the forwarder collects or pays money on behalf of the customer or a third party. If the charge carries a markup and represents a service Hai Long is selling to the customer, treat it as a normal charge in the Charges guide instead.

Role |

Task |

Verification needed |

|---|---|---|

Sales / Sales Ops |

Mark on-behalf lines on the quotation or sales order. |

On-behalf lines are not counted as service revenue. |

Operations |

Provide port/carrier documentation and notify the customer. |

Each amount to be recovered has source documentation and a responsible owner. |

Accounting |

Verify invoice, vendor bill/payment, and outstanding receivables. |

Gross profit does not inflate or go negative due to pass-through amounts. |

Distinguishing a normal charge from an on-behalf payment¶

Question |

Normal charge |

On-behalf / pass-through |

|---|---|---|

Does Hai Long add a markup? |

Yes, or Hai Long sets the selling price. |

No — recovery is for the exact amount paid or billed by the third party. |

Is this a service Hai Long is selling? |

Yes — e.g. ocean freight margin, handling fee. |

No — e.g. tax, port fee, third-party charge passed through unchanged. |

Should this appear in gross profit? |

Yes. |

No — it should not affect service gross profit. |

If the third party increases the fee, who bears the difference? |

Hai Long, if the selling price was already fixed. |

The customer, if the contract states actual-cost reimbursement. |

In the Saigon Export scenario:

Ocean Freight: buy USD 850, sell USD 1,050 → normal charge, margin USD 200.

THC USD 1,200, Fumigation USD 600, Detention USD 1,200 — recovered at exact cost → on-behalf / pass-through.

Step 1: Mark on-behalf lines on the sales order¶

Open the quotation or sales order for the Saigon Export shipment. In the Order Lines tab, keep the Ocean Freight line as a normal service line. For the three advance charges, mark each one as Mark On-Behalf and set the Collection Partner to Saigon Export Co., Ltd. — the customer who will reimburse Hai Long.

Line on sales order |

Amount |

Mark On-Behalf |

Collection Partner |

|---|---|---|---|

Ocean Freight |

USD 800 (or agreed selling price) |

No |

Leave blank |

Terminal Handling Charge — Cat Lai |

USD 1,200 |

Yes |

Saigon Export Co., Ltd. |

Fumigation Fee |

USD 600 |

Yes |

Saigon Export Co., Ltd. |

Container Detention — 5 days |

USD 1,200 |

Yes |

Saigon Export Co., Ltd. |

Mẹo

Step 1 is complete when:

The three lines for THC, Fumigation, and Detention each show Mark On-Behalf.

Collection Partner is the customer or the partner who will reimburse the advance.

The total on-behalf amount is USD 3,000.

The Ocean Freight line is not marked as on-behalf — it is Hai Long's service revenue.

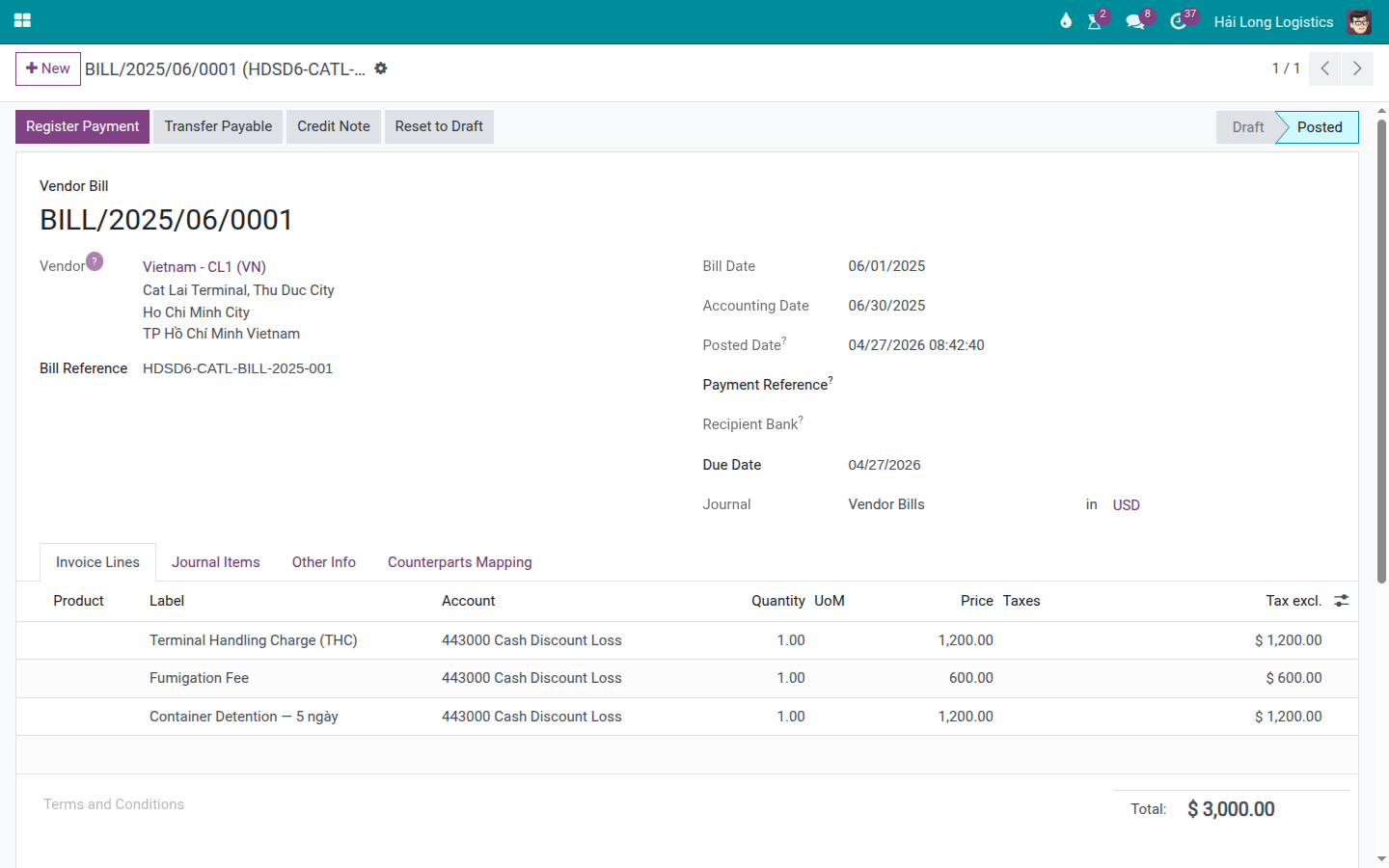

Step 2: Record the payment made or the third-party document¶

When Hai Long advances money to the port, customs authority, or carrier, Accounting needs the source documentation to reconcile against the recovery amount. For the Cat Lai scenario, create or record the vendor bill for the port charges at the actual amounts paid:

THC: USD 1,200.

Fumigation: USD 600.

Container Detention: USD 1,200.

Cảnh báo

Do not enter pass-through amounts as a service cost on the shipment if your company separates pass-through funds from gross profit. If entered incorrectly, the shipment may show negative profit (advance recorded as cost but no recovery) or inflated profit (recovery recorded as revenue without a matching cost). Both misrepresent the shipment's actual performance.

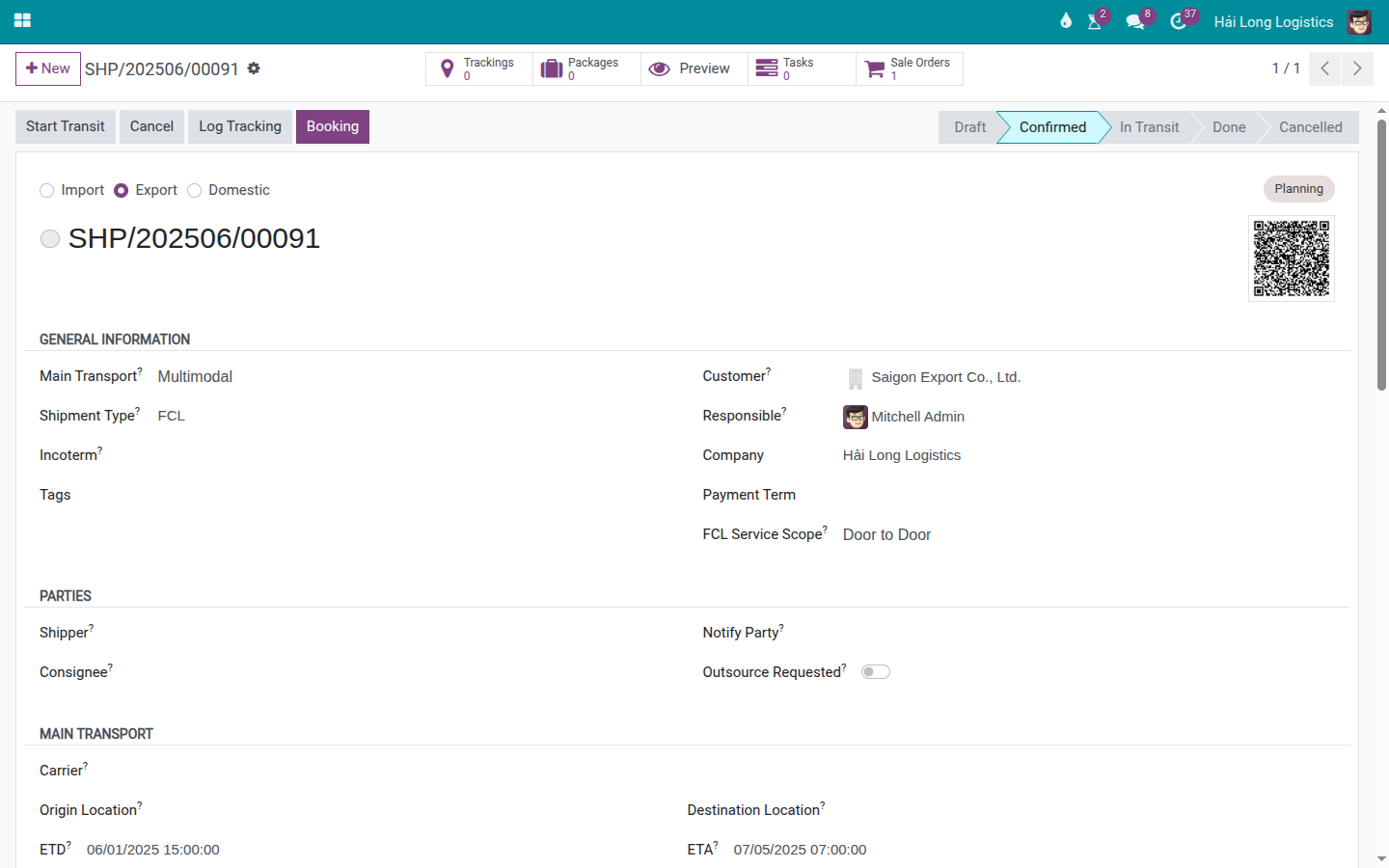

Step 3: Verify on the shipment and invoice¶

Open the shipment linked to the sales order. Verify:

The linked sales order shows the three on-behalf lines marked correctly.

The shipment or profitability section does not add the USD 3,000 to the service gross profit.

When creating the standard service invoice, the on-behalf lines are not treated as markup revenue if your process separates pass-through invoicing from service invoicing.

Mẹo

Step 3 is complete when:

Gross profit on the shipment reflects only the portion of revenue where Hai Long has a margin.

The total amount still to be recovered from Saigon Export remains USD 3,000.

Source documentation or notes explain each on-behalf amount.

Step 4: Track recovery from the customer¶

After sending documentation to the customer, Accounting monitors until the full advance is reimbursed. For Saigon Export, the recovery target is USD 3,000. When the customer pays, record the payment per your accounting process and allocate it to the corresponding on-behalf line if the system requires it.

Ops and Sales support Accounting by preserving the following documentation:

Bill or receipt from the port authority or carrier.

Email or written confirmation that the customer agreed to bear the charge.

Notes on the shipment identifying which lines are on-behalf and which are service fees.

Cảnh báo

Unrecovered advance payments are company funds sitting with the customer. Do not wait until month-end to check. Review open on-behalf balances as soon as a shipment is marked Done or immediately after sending documentation to the customer — whichever comes first.

On-behalf payments in sea import¶

For sea import shipments, Hai Long may advance import duties, D/O fees, storage fees, or quarantine charges to release cargo on the customer's behalf. The handling is identical to the export scenario:

Identify which amounts the customer owes and Hai Long is only advancing.

Mark those lines as Mark On-Behalf on the sales order.

Set Collection Partner to the customer who will reimburse.

Preserve the payment voucher or third-party receipt.

Verify that the pass-through amounts do not affect the shipment's service gross profit.

Troubleshooting common situations¶

Situation |

Common cause |

Resolution |

|---|---|---|

Gross profit is unusually high. |

On-behalf amounts were entered as service revenue. |

Mark the lines as Mark On-Behalf, review any invoices already issued, and correct per your accounting process. |

Gross profit is unusually negative. |

Advance amounts were recorded as cost without a matching recovery line. |

Separate the pass-through from normal charges, or add the corresponding on-behalf recovery line. |

Collection Partner is blank. |

No one has been identified to reimburse the advance. |

Fill in the customer or partner responsible for the charge before closing the shipment. |

Customer has not reimbursed. |

Documentation not sent, receivable not followed up, or payment not allocated correctly. |

Resend the source documentation, follow up on the receivable, and update the payment allocation per your Accounting process. |

VAT/tax does not match the source document. |

The on-behalf line does not reflect the exact gross amount billed by the port or carrier. |

Confirm with Accounting whether the recovery is pre-tax or inclusive of tax; adjust before issuing the document to the customer. |

On-behalf section does not appear on the shipment. |

Module not installed, configuration incomplete, or the sales order is not properly linked to the shipment. |

Check that the sales order is linked to the shipment and that the lines are marked correctly; if the section is still missing, use the sales order as the primary reference. |

Final checkpoint¶

Before closing a shipment that has on-behalf payments, verify:

Every pass-through amount is correctly marked on the sales order.

Collection Partner is the party who will reimburse.

Source documentation from the third party has been saved.

Invoice and gross profit do not include pass-through amounts as markup revenue.

The outstanding recovery amount has an assigned owner tracking it to completion.

Xem thêm

Related guides

Charges and Profitability — Review charges and shipment gross profit.

FCL Export — Sea FCL export where THC, detention, and fumigation are common on-behalf items.

FCL Import — Sea FCL import where D/O fees, customs duties, and storage are common on-behalf items.